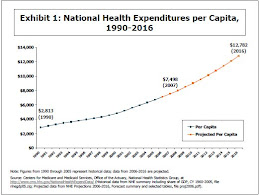

I believe it's so difficult to determine exactly what is contributing to the rising costs of healthcare that any research that definitively points to any particular factor is probably suspect. Han Tun cited the report by Ginsberg via the Robert Wood Johnson Foundation (which is an excellent and comprehensive study that I would highly recommend reading), and even though his well-constructed analysis leads him to the conclusion that medical technology is one of the major contributors to rising healthcare costs, Ginsberg notes in his conclusion that, "the area covered by this synethesis that is least understood is medical technology...the process of selecting technologies [to study] is so unstructured so as to leave real concerns about how representative those technologies are."

Rather than trying to pinpoint specific factors, which will only lead to specific reforms, I feel that it is more constructive to examine the fundamental economics behind healthcare spending, which will lead to broader, more comprehensive reforms.

Health economics can get exceedingly complex (with lots of very awesome math), but let's just whittle it down to a very simplistic thought experiment that will flesh out the major issues:

The thriving nation of Example consists of 100 people. The people are divided into two populations: the healthy and the sick. At any given time, there is a dynamic equilibrium where 10 are sick and 90 are healthy (that is, some of the 10 sick people will eventually become healthy, but they will be immediately replaced by some healthy people that become sick. Crucially, the sick population does not always consist of the same 10 people).

There is only one sickness: skin cancer. It is non-contagious but cannot be resolved without significant medical intervention. The cost of curing skin cancer is $1,000. Everyone in the nation earns an identical income of $500 per year.

Right away, the fundamental challenge of healthcare financing is apparent: if the cost of treating skin cancer is twice as much as what any single individual can pay in a year (even if they spent their income on healthcare and nothing else), then how can anyone afford to become healthy?

Let’s say the nation as a whole makes two assumptions at this point:

The cost of treating sickness cannot be significantly reduced from $1,000.

At any given time, 10 people in the nation will be sick (and this number cannot be reduced).

Under these two assumptions, the only solution is for the sick to use other people’s money to pay for treatment.

This is where the health insurance system comes in. Its existence is justified by the inability of a single individual to pay for the cost of treating his own illness. Instead, risk is pooled; that is, everyone pays into an insurance fund to which any of them can lay claim once they become sick. All 100 people in the nation have an incentive to obtain insurance because any one of them could become a member of the sick population at any time, without warning. Under a perfect insurance system, the cost of the treating the sick ($1,000 x 10 people, or $10,000) will at any given time be distributed among 90 healthy payers (only $111 per person, which can be paid out at a rate of $3/year per person for 37 years).

Because health insurance is a service like any other service in Example’s economy, people have a choice between different types of insurance, and can also choose to have no insurance at all. However, because they are given a choice to obtain insurance, it is only fair that insurance companies have the corresponding choice to accept or reject people from their pool to prevent abuse of the system (via certain prerequsites like the lack of a preexisting condition).

Let’s see if we can predict how costs will be shifted under this system.

First, let’s figure out what happens to the basic supply-demand model behind treating skin cancer. Now the people of Example no longer pay their doctors for their services. Rather, the people pay an intermediary--the insurance company--who then pays the doctors. The people of Example are, in other words, insulated from the potential cost of their care. What the sick population of Example sees on their bills is not $1,000 (the real cost), but installments of $3 (their insurance premium). As the real cost ($1,000) changes over time due to inflation or provider supply, the premium will not be able to adjust immediately. In time, it will no longer be perfectly representative of reality.

Now let’s reexamine the incentive for the healthy people to purchase insurance. Their onlyyou would fall in that 10% in your lifetime? Or maybe you feel that there are bigger and better things to pay for, like a flat screen television, or your child’s education. Or maybe all those different plans seem too complicated, and you can’t bother to buy something you don’t even understand. Or it just seems too expensive. Or whatever. incentive is that there is a possibility that they may contract skin cancer. But how likely is that? After all, only 10% of Example is sick at any time. As a citizen of Example, what are the chances that

So you decide to risk it. You don’t buy into the insurance pool, or you buy into it much later, such that you only pay $3/year for 10 years instead of the full 37. As a result, the cost for the remaining 89 individuals to buy into the pool increases marginally. This initiates the vicious cycle that's the bane of every insurance system ever conceived: you decide not to pay, so the cost of insurance increases. The cost of insurance increases, so other people decide not to pay. And so on, and so forth.

There is a solution for this problem that can compensate for Example’s insulation from healthcare costs and prevent the vicious cycle from beginning in the first place. The solution is obvious and fairly simple: mandate insurance. In this way, everyone buys into one insurance plan or another the moment they are born, and pays their dues until they get sick. If they aren't yet sick, then their contributions are used to treat those who are currently sick.

There is no denying that healthcare is subject to the same market forces as any other service. If this is the case, then we need to find a way to make the market function properly, such that supply and demand are matched through adequate competition or price negotiation. There are many, many ways to do this, but they all attempt to compensate for the consumer's insulation from the cost of care. This, I feel, is the fundamental problem in healthcare financing, and the best solution (whatever it is) will address this first, rather than point to a specific cause (technology, administrative inefficiency, etc.).

No comments:

Post a Comment